Life is a four-letter word for a reason: It gets difficult at times and the unexpected is almost certain to occur at some point.

That’s why having an emergency fund is so important but usually it’s not enough. That’s where insurance comes in.

Insurance is a contract between you and an insurance company.

You pay them a certain amount of money regularly (called premiums), and in return, if something bad happens, they help you and/or your family with a tax free, lump sum of money. This can apply to a critical illness, disability, death etc. Different types of insurance are more appropriate in different situations. Ask us which is best for you!

Private Reserve Strategy/Emergency Fund

We can help you become your own bank with our Private Reserve Strategy.

Julie's Story

When Julie started out as a financial advisor, she realized that traditional financial planning doesn’t cover everything. When her kids were babies, she got sick and was misdiagnosed with Cancer. Those were scary times!

Even though she was supposedly doing everything right – an emergency fund, quick paying her mortgage and building retirement assets – things almost didn’t work out.

She was misdiagnosed with Lymphoma/cancer and thankfully she didn’t actually have it. She wanted to increase her odds of survival and looked into a great treatment that would cost over $100,000 US dollars. That’s when she realized that she didn’t have access to her hard-earned money.

She would have to qualify at the bank to access the equity in her home and the bank wouldn’t lend money to someone who may be dying. She could take money from her RRSP but given that it all gets added to your income, she’d have to take out over $200,000 to net $100,000. That’s a lot of money, especially 25 years ago when you have a young family.

Julie had an emergency fund but not enough money for that emergency.

Critical illness could have covered Lymphoma, but when they found it wasn’t lymphoma, her condition wasn’t covered through critical illness coverage, so she needed to find cash elsewhere.

Julie realized that she did not have access to capital, or as she now says “LUCK“. Liquidity, Use, Control and Knowledge about her money.

She quickly learned that building your net worth is important buthaving access to capital is critical in order to have freedom, opportunity and control! RRSP’s and Real estate are not the best place to build liquidity.

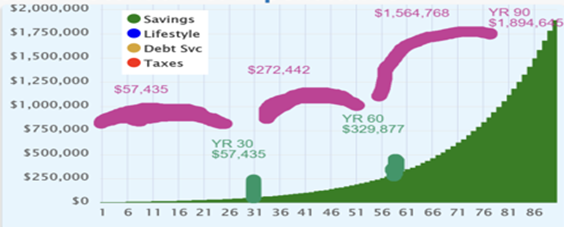

Everyone knows that compounding is amazing.

That’s when money grows exponentially on itself. But that only happens when the money is left to compound uninterrupted in a tax-free account, using investments that never go down in value.

When you look at the curve above, you realize that the first years have very little growth and most of the growth happens in the later years. See how compounding really takes off in the last 30 years, assuming you have never redeemed and you’ve only had positive returns. The last 30 years is where you get the “hockey stick curve” that everyone talks about.

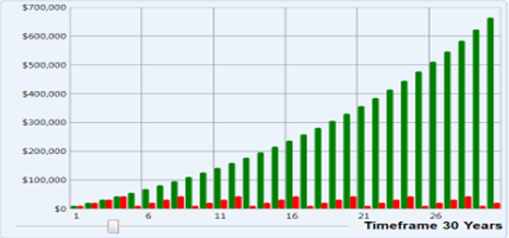

If you let your money grow in a tax-free savings account, every time you redeem money, even if you pay it back with interest (the red graph), you are basically restarting the compounding curve. This is costing you a fortune!

As you can see if you had let the money compound you would have more like the green line, versus the red line results.

Are you cutting down your financial tree every time you redeem money?

Or are you just taking your financial “apples” and allowing the tree to grow!

Think of it this way

You’re hungry, and you’re craving some juicy apples. Now, imagine emptying your investment account is like chopping down the entire apple tree just to grab a few apples. But here’s the catch—you’ll have to plant a new tree and wait for years before you can enjoy the fruits of your labor (ie. the slow growth in the first years).

Instead of that hassle picture this…

You pluck the apples (or in our case, let your money grow tax-free, and then you take out a loan and pay it back). The result? You’ll end up with way more money in the long run. The GREEN graph versus the RED graphs.

Not only that, but you’ll always have a stash of cash (your Private Reserve) on hand for life’s unexpected twists, because you can count on having access to your money.

Oh, and it’s also a smart move for your retirement plan, plus whatever’s left behind will pass on to your heirs without tax. Unlike with the TFSA, your early death will be a financial jackpot since with insurance you get a significant multiplier effect.

Clearly, we’re not talking about your run-of-the-mill tax-free savings account here. If you want to dive deeper into setting up your own private reserve strategy, just ask!